By Phil Kerpen

Before Republicans agreed to elect Kevin McCarthy Speaker of the U.S. House of Representatives, a handful of his colleagues demanded the implementation of a fiscal framework to rein in federal spending.

The threat of spending reduction has, however, launched a full debt ceiling “default” panic. The spending interests are trying to cast conservatives as unreasonable and spendthrift Democrats as saviors of our economy for favoring no-strings-attached increases in federal debt.

In the Orwellian world of Washington, the media and other Democrats call what they want a “clean” debt ceiling increase. But what could be dirtier than jacking up the limit on the national credit card with no plan to reform spending?

The rhetorical strategy they deploy to continue reckless spending is to insist the alternative to a naked debt ceiling increase is “default.” But a federal debt default is not a risk as long as there is more money coming into the federal government on a monthly basis than is owed in interest.

Over the past decade, paying interest on the debt consumed about 10 percent of monthly federal revenues, and in no month reached 20 percent. That means a scenario in which Congress does not raise the debt ceiling and the federal government is forced to operate on a cash basis presents no genuine risk of default.

It would be massively disruptive – much of the government would necessarily shut down and bills would not be paid in a timely fashion. But defaulting on the debt would not occur unless Treasury made the irrational decision not to pay bondholders with current revenue.

So-called experts who insist on “correcting” politicians who refer to a debt ceiling lapse as a shutdown are wrong, and Congress could take this deception off the table by passing a law clarifying that Treasury is required to pay bondholders first.

But while the “default” crisis from a lapse in the authority to issue additional debt is fake, the risk of a real debt crisis is visible on the horizon.

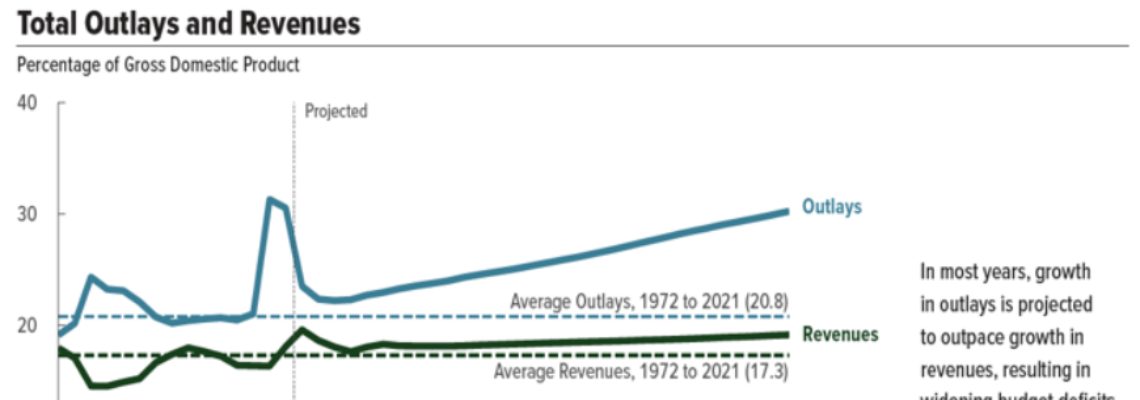

The latest long-term budget projections from the Congressional Budget Office show debt reaching a new all-time high of 107 percent of GDP in 2031 and soaring to 185 percent of GDP in 2052. This is driven almost entirely by federal spending, which is expected to remain higher than before the pandemic even after much of the one-time spending ends. Spending then significantly rises starting in 2025 until it reaches 30.2 percent of GDP in 2052.

Revenues for 2022 came in at 19.6 percent of GDP, the second highest level ever recorded – contrary to the predictions of Trump tax cut opponents – and projected revenues are expected to remain well above the historical norm of 17.3 percent of GDP and remain in the 18 to 19 percent range.

Congress must restrain federal spending before we face a real debt crisis in which we actually cannot afford to pay our bills.

Every major spending and debt deal in Congress since 1985’s Gramm-Rudman-Hollings Act has included negotiations over the debt ceiling. House conservatives were right to demand spending reforms as a condition for raising the debt, and they should hold firm even if it means a government shutdown. The only clean outcome is one that sets spending on a more sustainable path.